Buying a home can save you 10s of thousands of dollars in income tax payments while also allowing you to make hundreds of thousands of dollars in untaxed capital gains on the sale of your primary residence.

Should You Itemize Your Income Taxes?

Use this calculator to find out how much your potential interst-expense income tax deductions are and if it makes sense to itemize your taxes.

Please note that tax policies can & do change. This tool should be used for informational purposes only & you should contact your financial advisor before making any big financial decisions.

We publish current El Monte mortgage rates to help you compare any quoted rates you received against competitive rates from our online network of mortgage lenders.

Calculate Your Home Ownership Tax Benefits

2025 Tax Changes

The One Big Beautiful Bill tax legislation was signed into law by President Trump on July 4, 2025.

The new bill increases the state and local tax (SALT) deduction from $10,000 to $40,000.

If tax filers have an adjusted gross income above $500,000 then the $40,000 limit is reduced by 30% of the income above $500,000, with a floor deduction amount of $10,000.

From 2026 to 2029 the higher SALT cap and the $500,000 income threshold will be increased by 1% annually.

| Year | SALT Limit | Income Threshold |

|---|---|---|

| 2025 | $40,000 | $500,000 |

| 2026 | $40,400 | $505,000 |

| 2027 | $40,804 | $510,050 |

| 2028 | $41,212 | $515,151 |

| 2029 | $41,624 | $520,302 |

As the SALT limit goes up by a maximum of $1,624 and the income level goes up about 4% total we used the 2025 limits for all years, as we do not know how your income will change in out years and the math gets a bit complex if we guess your wages, your future state income taxes, and ultimately we are talking about saving at most $601 (37% of %1,624) for doing a lot of fuzzy and complicated math with many guestimates in it, plus the shifts would be in nominal Dollars rather than real spending power.

What Happens in 2030?

After 2029 the SALT deduction cap will revert to $10,000, unless the current law is once again renewed to extend the higher caps. The calculation below presumes the $40,000 limit will be renewed.

* For now, states which allow pass through entity taxes still have full deduction of state and local taxes paid through pass through entities. Even if the lower limit is reverted to the pass through entity exemption is likely to remain.

2018 Changes to Mortgage Interest Income Tax Deduction

Congress passed the Tax Cuts and Jobs Act of 2017, which changed the tax code in a number of ways that limits the breadth of income-tax deductions tied to homeownership.

- Lower cap on deductable debt: The amount of mortgage debt upon which interest is deductable from income taxes has been lowered. The old limit was $1,000,000 and the new limit is $750,000.

- Increase standard deductions: In 2018 they increased standard deductions to $12,000 for individuals or married couples filing individually, $18,000 for heads of household & $24,000 for married couples. In 2025 these standard deductions jumped to $15,000, $22,500 and $30,000 respectively. Over the 7 years that equates to a 3.24% CAGR.

- Cap on SALT deductions: State and local taxes were fully deductible from income in prior years. From 2018 onward there is a deduction cap of $10,000 for state and local taxes. High earners who pay significant property taxes in states with high property values & relatively high state income taxes like California, New York or New Jersey will frequently spend over $10,000 on state and local taxes, meaning they are only able to deduct a portion of their local income & property taxes.

Grandfathering of Older Mortgages

The legislation lowering the deductibility of mortgage interest is reflected in the tax code from 2018 onward, with older existing loans grandfathered into the limit of being able to deduct points & interest payments on up to $1,000,000 in mortgage debt. If your mortgage was in place before this law is enacted you get grandfathered into the old higher limit. If you refinance your mortgage after the new law is in place, then the mortgage refinance loan will still be grandfathered into the old limit since the first mortgage it is replacing qualified for the old limit. If some of the refinance was used to "cash out" equity then only interest on the portion of the loan which did not add to the original debt amount would be tax deductible on a pro-rated basis.

Interest on second mortgages, which are usually structured as home equity loans or HELOCs, is no longer tax deductible unless the loan was taken out to substantially improve or expand upon your main home. If you deduct second mortgage interest be sure to keep receipts in case yoou are audited.

This calculator currently defaults to the $750,000 limit. If your first mortgage closed before 2018 & your loan is above $750,000 then please uncheck on the "Use current limit" checkbox to use the old limit.

Estimated Mortgage Interest Tax Deduction Savings on a 7.0% APR 30-Year $320,000.00 Fixed Rate Mortage

For the sake of simplicity this calculator presumes no changes to tax laws in terms of the SALT deduction cap. The estimated standard deduction in future years changes at the annual rate you entered in the calcualtor's "annual inflation adjustment" setting, which defaulted to 3.24% - the CAGR between 2018 and 2025. Each year the standard deduction tend to grow slightly to offset the impacts of inflation, though the further you go out in time the more uncertainty there is in the tax laws and inflation rates at that point in time.

| Year | Interest | SALT | Other | Total | Standard | Difference | Itemized Savings |

|---|---|---|---|---|---|---|---|

| 1 | $28,697.02 | $40,000.00 | $2,000.00 | $70,697.02 | $30,000.00 | $40,697.02 | estimated savings: $14,243.96 |

| 2 | $22,062.04 | $40,000.00 | $2,000.00 | $64,062.04 | $30,972.00 | $33,090.04 | estimated savings: $11,581.51 |

| 3 | $21,810.07 | $40,000.00 | $2,000.00 | $63,810.07 | $31,975.49 | $31,834.58 | estimated savings: $11,142.10 |

| 4 | $21,539.88 | $40,000.00 | $2,000.00 | $63,539.88 | $33,011.50 | $30,528.38 | estimated savings: $10,684.93 |

| 5 | $21,250.16 | $40,000.00 | $2,000.00 | $63,250.16 | $34,081.07 | $29,169.09 | estimated savings: $10,209.18 |

| 6 | $20,939.50 | $40,000.00 | $2,000.00 | $62,939.50 | $35,185.30 | $27,754.20 | estimated savings: $9,713.97 |

| 7 | $20,606.37 | $40,000.00 | $2,000.00 | $62,606.37 | $36,325.30 | $26,281.07 | estimated savings: $9,198.37 |

| 8 | $20,249.17 | $40,000.00 | $2,000.00 | $62,249.17 | $37,502.24 | $24,746.93 | estimated savings: $8,661.42 |

| 9 | $19,866.15 | $40,000.00 | $2,000.00 | $61,866.15 | $38,717.31 | $23,148.84 | estimated savings: $8,102.09 |

| 10 | $19,455.43 | $40,000.00 | $2,000.00 | $61,455.43 | $39,971.76 | $21,483.67 | estimated savings: $7,519.29 |

| 11 | $19,015.03 | $40,000.00 | $2,000.00 | $61,015.03 | $41,266.84 | $19,748.19 | estimated savings: $6,911.87 |

| 12 | $18,542.79 | $40,000.00 | $2,000.00 | $60,542.79 | $42,603.89 | $17,938.90 | estimated savings: $6,278.62 |

| 13 | $18,036.41 | $40,000.00 | $2,000.00 | $60,036.41 | $43,984.25 | $16,052.16 | estimated savings: $5,618.26 |

| 14 | $17,493.42 | $40,000.00 | $2,000.00 | $59,493.42 | $45,409.34 | $14,084.08 | estimated savings: $4,929.43 |

| 15 | $16,911.18 | $40,000.00 | $2,000.00 | $58,911.18 | $46,880.60 | $12,030.58 | estimated savings: $4,210.70 |

| 16 | $16,286.85 | $40,000.00 | $2,000.00 | $58,286.85 | $48,399.54 | $9,887.31 | estimated savings: $3,460.56 |

| 17 | $15,617.39 | $40,000.00 | $2,000.00 | $57,617.39 | $49,967.68 | $7,649.71 | estimated savings: $2,677.40 |

| 18 | $14,899.54 | $40,000.00 | $2,000.00 | $56,899.54 | $51,586.63 | $5,312.91 | estimated savings: $1,859.52 |

| 19 | $14,129.79 | $40,000.00 | $2,000.00 | $56,129.79 | $53,258.04 | $2,871.75 | estimated savings: $1,005.11 |

| 20 | $13,304.39 | $40,000.00 | $2,000.00 | $55,304.39 | $54,983.60 | $320.79 | estimated savings: $112.28 |

| 21 | $12,419.33 | $40,000.00 | $2,000.00 | $54,419.33 | $56,765.07 | -$2,345.74 | below standard deduction |

| 22 | $11,470.28 | $40,000.00 | $2,000.00 | $53,470.28 | $58,604.26 | -$5,133.98 | below standard deduction |

| 23 | $10,452.63 | $40,000.00 | $2,000.00 | $52,452.63 | $60,503.04 | -$8,050.41 | below standard deduction |

| 24 | $9,361.41 | $40,000.00 | $2,000.00 | $51,361.41 | $62,463.33 | -$11,101.92 | below standard deduction |

| 25 | $8,191.31 | $40,000.00 | $2,000.00 | $50,191.31 | $64,487.15 | -$14,295.84 | below standard deduction |

| 26 | $6,936.62 | $40,000.00 | $2,000.00 | $48,936.62 | $66,576.53 | -$17,639.91 | below standard deduction |

| 27 | $5,591.23 | $40,000.00 | $2,000.00 | $47,591.23 | $68,733.61 | -$21,142.38 | below standard deduction |

| 28 | $4,148.58 | $40,000.00 | $2,000.00 | $46,148.58 | $70,960.58 | -$24,812.00 | below standard deduction |

| 29 | $2,601.64 | $40,000.00 | $2,000.00 | $44,601.64 | $73,259.70 | -$28,658.06 | below standard deduction |

| 30 | $942.88 | $40,000.00 | $2,000.00 | $42,942.88 | $75,633.31 | -$32,690.43 | below standard deduction |

Want to Save Even More? Lock-in Today's Low Mortgage Rates ! |

|||||||

Current El Monte Mortgage Rates for a 30-year Fixed $320,000 Home Loan

The following table highlights current El Monte mortgage rates. By default 30-year purchase loans are displayed. Clicking on the refinance button switches loans to refinance. Other loan adjustment options including price, down payment, home location, credit score, term & ARM options are available for selection in the filters area at the top of the table.

Understanding the Tax Benefits of Home Ownership

Interest is the fee you pay your lender for the use of their money. All debts have them, and mortgages are no exception. Mortgages are unique in that they have tax advantages. You can write off the cost of your home’s mortgage in your tax returns. In essence, you are getting your money back. This key advantage is one of the most attractive aspects of home ownership.

The rules may change, but the benefits remain the same. Leveraging mortgage interest does more than reduce your tax burdens. It also gives you back the interest you paid on your home. And this isn’t the only tax benefit you get from a mortgage. Since your home is also your biggest major investment, it also has a few other tax benefits down the line.

Defining Mortgage Interest

You don’t receive any tax benefits from consumer debts like car loans or credit card bills. This benefit is unique to homeowners with mortgages. But not all mortgages apply. Mortgage interest refers to the interest you pay to your home mortgage. This is the money you used to pay for any property you own that serves as your primary residence.

It may also refer to the interest from the following debts.

- Secondary mortgage: Any money you borrow to buy a second home.

- Refinanced mortgage: A new loan used to pay off your old mortgage. This is often used to help you switch to more favorable terms of payment.

The common thread of these loans is that they are secured by your home. Should you default on your payments, your lender forecloses on the property.

The IRS is quite strict on what mortgage debts qualify as deductibles. What they’re more lenient on is the type of property involved. Any type of residential property can qualify for an interest deduction, be it house or condo. The rules that govern how much you can write off, however, vary.

You have an upper limit to how much you can deduct on your primary and secondary residences. But what makes a “residence” what it is? Separating a secondary residence from an investment can be tricky for the layperson.

Residences and Rentals

The primary (or principal) residence is easy enough to understand. It is where you live for much of the year. It is also the address where you receive your mail. A second home is a property that serves as your residence for part of the year. Most second homes are vacation homes, and the definition is built around that. Some of the rules that govern second homes are as follows:

- Your family must be its primary occupants.

- In many cases, your property must be found a specific distance from your primary residence. Others define second homes as properties located specifically in vacation destinations.

- Renting it out must be a secondary consideration. Some lenders actively discourage buyers from renting out their second homes in their mortgage agreements.

You can have several “second” homes. Any subsequent property you buy counts as long as they meet these criteria. People sometimes use the term investment property to refer to second homes. For tax purposes, however, the two have strict legal distinctions. An investment property is any piece of real estate you buy with the intention of profiting from it. This umbrella term includes vacation rentals, residential rentals, and fix-and-flip homes.

While you can rent out a second home, you must follow specific rules to do so. The Internal Revenue Service (IRS) defines the following conditions to distinguish between the two:

- You and your family must use the property for at least 14 days in a year, or

- You and your family spend 10 percent or more of the time it was occupied by tenants.

The IRS counts a home as an investment property or a second home based on the greater option that applies. Suppose you rent out your home for 170 days. You and your family must stay there for 17 days for the property to count as a second home.

If you rent your home out for two weeks or less, you need not pay taxes on your rental income. The distinction, however, becomes important the longer you rent out the property. Rent revenues from rentals and second homes are taxable if you rented them out for longer than 2 weeks. Your second home can qualify for mortgage interest tax deduction if it fits the bill. This can offset the taxes on your rental income.

Besides mortgage interest deductions, rental properties have other tax benefits. You may also take advantage of other costs to write off as business expenses. You can even defer capital gains taxes through a 1031 exchange. This helps you manage the tax burdens of reinvesting in real estate.

A Note on HELOCs

You should not confuse mortgages for second homes with second mortgages. These come in two forms: home equity loans and home equity lines of credit (HELOCs). Like regular mortgages, your HELOC is backed by the value of your home. Lenders secure them through home equity, the percentage of your home that you’ve paid for.

These are distinct from mortgages as a product, though they are still related. Although they are also tax deductible, HELOCs are governed by a different set of rules. You can only deduct taxes from HELOC if you use funds from the loan to build or significantly improve your home. Any other expense, such as paying for college tuition, car repairs, or other costs are not tax deductible.

Itemized Deductions

The U.S. tax system rewards long-term reinvestment. Mortgage interest tax deductions eases one major burden of buying a home on debt. By writing off your interest, you keep more of your money for other uses. That’s money you can spend on your needs, wants, or debt payments. You can deduct your mortgage interest in one of two ways:

- The standard deduction

- Through an itemized deduction

In the past, itemized mortgage interest deductions were a popular tax exemption. You often had to make separate calculations for your mortgage interest. However, homeowners woke up to a new tax reality in 2018. The Tax Cuts and Jobs Acts (TCJA) of 2017 had a profound impact on the way people filed taxes.

On the whole, it simplified the filing process for many taxpayers. They no longer needed to itemize tax deductions, which could become costly. Instead, they can file for the now-doubled standard deduction. But this simplification also came with major changes. One of the deductions affected by the TCJA were those for mortgage interest. The new rules lowered the size of the mortgages eligible for itemized deductions. Here are the major changes:

| Demographic | Pre-TCJA Cap | Post-TCJA Cap |

|---|---|---|

| Married Filing Jointly | $1,000,000 | $750,000 |

| Single and Married Filing Separately | $500,000 | $375,000 |

These only apply to mortgages taken out between 2018 and 2025. By then, Congress will once again review tax rules. The old deductions still apply for homeowners who took out their mortgages before the 14th of December 2017.

The new deductions mean that homeowners don’t always need to itemize interest costs. Much of their mortgage interest could fit with the new deduction. The new caps will affect owners of larger or several homes, which tend to be on the expensive side. People who took out million-dollar mortgages cannot write off their interest payments anymore.

Among the many provisions preserved by the TCJA were deductions for second homes. These are identical for those you took for your primary residence.

Deductibles Through The Years

Since 2018, the federal government grants tax payers a higher annual standard deduction. These vary depending on your marital and family status. In 2025 they are:

- $15,000 for single taxpayers

- $22,500 for heads of households

- $30,300 for those married filing jointly

- $15,000 for those married filing separately

- $30,000 for a qualified widow(er)

For your mortgage to qualify for an itemized deduction, it must exceed this cap. Many individual homeowners will not qualify for itemization. Long-time homeowners no longer pay enough interest to justify itemizing. Often, their interest costs can fall into the new standard deduction.

The best time to itemize your interest payments is in the earlier years of your mortgage. In this period, most of your monthly payments go toward interest. Over time, more of your payments go toward principal. Once you start paying more principal, your interest payments become smaller.

Let’s see this in action using our calculator above. Suppose you bought a home worth $450,000. You paid a 20 percent down payment, which is $90,000. Your mortgage has a term of 30 years and an annual percentage rate (APR) of 4.5 percent. We will assume the following details:

- You and your spouse file jointly.

- Together, you fall under the 22 percent federal income tax bracket.

- Each year, you have about $15,000 worth of deductible expenses.

- This example was calculated a few years back when standard deductions were lower and interest rates were much lower. Please use the current calculator to run your numbers.

30-Year Fixed Rate Mortgage

Principal: $360,000

Rate: 4.5%

| Year | Interest | Other | Total | Standard | Difference | Itemized Savings |

|---|---|---|---|---|---|---|

| 1 | $16081.19 | $15000.00 | $31081.19 | $25100.00 | $5981.19 | estimated savings: $1,315.86 |

| 2 | $15814.39 | $15000.00 | $30814.39 | $25100.00 | $5714.39 | estimated savings: $1,257.17 |

| 3 | $15535.33 | $15000.00 | $30535.33 | $25100.00 | $5435.33 | estimated savings: $1,195.77 |

| 4 | $15243.45 | $15000.00 | $30243.45 | $25100.00 | $5143.45 | estimated savings: $1,131.56 |

| 5 | $14938.17 | $15000.00 | $29938.17 | $25100.00 | $4838.17 | estimated savings: $1,064.40 |

| 6 | $14618.86 | $15000.00 | $29618.86 | $25100.00 | $4518.86 | estimated savings: $994.15 |

| 7 | $14284.88 | $15000.00 | $29284.88 | $25100.00 | $4184.88 | estimated savings: $920.67 |

| 8 | $13935.55 | $15000.00 | $28935.55 | $25100.00 | $3835.55 | estimated savings: $843.82 |

| 9 | $13570.18 | $15000.00 | $28570.18 | $25100.00 | $3470.18 | estimated savings: $763.44 |

| 10 | $13188.03 | $15000.00 | $28188.03 | $25100.00 | $3088.03 | estimated savings: $679.37 |

| 11 | $12788.31 | $15000.00 | $27788.31 | $25100.00 | $2688.31 | estimated savings: $591.43 |

| 12 | $12370.24 | $15000.00 | $27370.24 | $25100.00 | $2270.24 | estimated savings: $499.45 |

| 13 | $11932.96 | $15000.00 | $26932.96 | $25100.00 | $1832.96 | estimated savings: $403.25 |

| 14 | $11475.59 | $15000.00 | $26475.59 | $25100.00 | $1375.59 | estimated savings: $302.63 |

| 15 | $10997.21 | $15000.00 | $25997.21 | $25100.00 | $897.21 | estimated savings: $197.39 |

| 16 | $10496.85 | $15000.00 | $25496.85 | $25100.00 | $396.85 | estimated savings: $87.31 |

| 17 | $9973.50 | $15000.00 | $24973.50 | $25100.00 | -$126.50 | below standard deduction |

Itemizing makes the best sense during the first few years of your mortgage. But the rewards of doing so diminish with each passing year. While you can save up to $1,315.86 in the first year alone, you only save $197.39 in 15 years. You save more money by switching to the standard deduction in 17 years. You may even start sooner if you reach the point where your savings are not worth the effort.

Home Equity Borrowing

Interest on HELOCs is another deductible modified by the TCJA. The 2018 changes preserved the old borrowing cap. If you are married and filing jointly, your cap is $100,000. For single people and those married filing separately, the cap is $50,000. New regulations put strict limits in how HELOCs can qualify as deductibles.

Before the TCJA, homeowners can write off interest from HELOCs used for any purpose. And use them they did. Homeowners can use home equity to finance cars or other expenses. You can even use HELOCs to consolidate debts. But back then, many would write off their interest to these debts as tax deductions. And not paying interest on these things is an attractive proposition.

Since 2018, the days where you can write off home equity interest for anything have passed. To qualify for deductions, you must only spend your HELOC on home improvements. Moreover, you must provide proof of this use when filing the deduction. As long as the TCJA is active, homeowners cannot write off HELOC debts used for any other purpose.

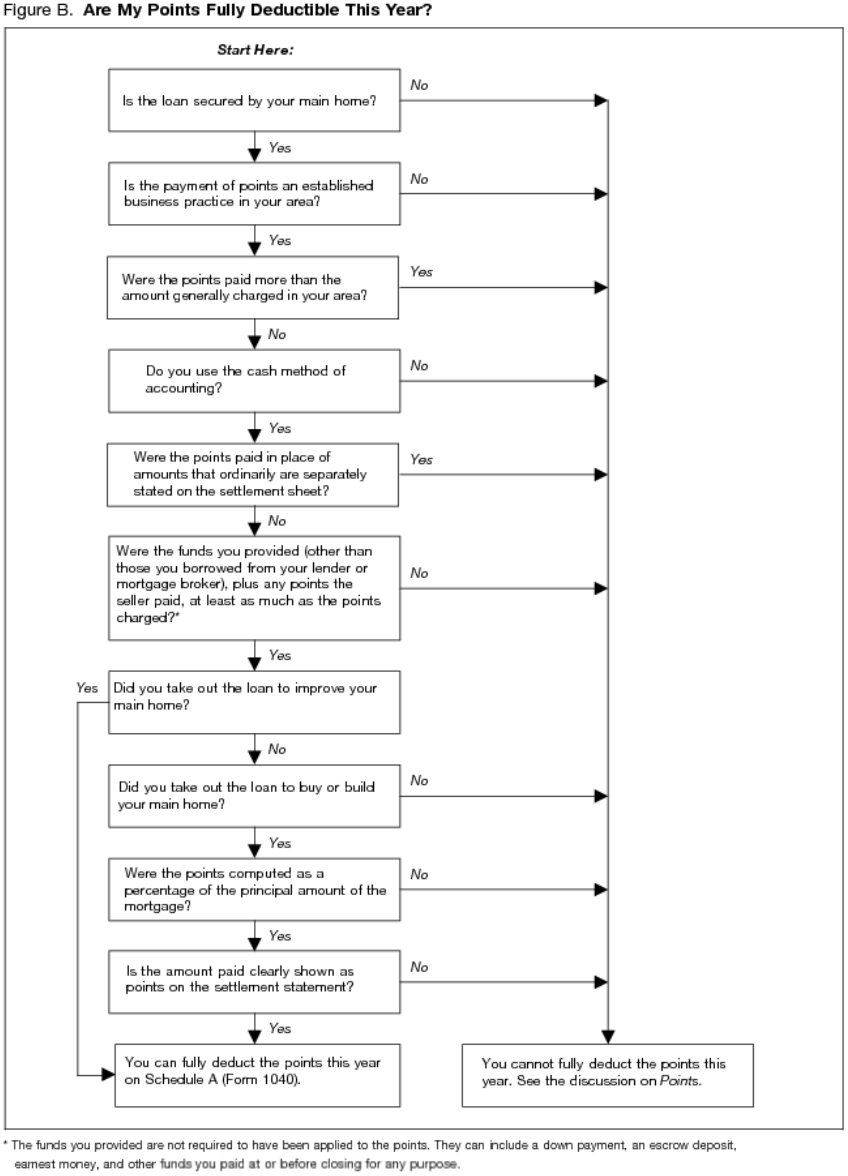

The Power of Points

Buying discount points help you lower the interest rate or other costs of your mortgage. By buying points, you save money in the long run at the cost of paying up front. Points are among the priciest optional closing costs you may encounter. Points cost a percentage of your mortgage loan amount, and lenders may offer you up to three points.

Points are, in essence, prepaid interest. Thus, they are also tax deductible. Points are deductible if you itemize your exemptions. You have the option of deducting them from your taxes in one of two ways:

- On a prorated basis throughout the amortization period

- In full during the year you took out the mortgage

Whether points are worth it depends on two factors. One is the length of time you plan to stay in your home. By lowering your APR, you can save thousands of dollars in interest cost over a long time horizon. They won’t save you much if you sell your home after a few years. Another is the general trend of interest rates. In times when the mortgage rates seem to only go up, it makes sense to buy them down. But if the rates trend downward, you may save more money from refinancing your mortgage.

Want to know whether your points can still count as deductible? This flow chart from the IRS’ Publication 936 can serve as a convenient guide:

Planning Around Taxation

Tax deductions aren’t the only benefit you can get from your home. Should you choose to sell your home, you can, with the right moves, save thousands of dollars in taxes. But be warned that it goes both ways. If you make the wrong set of choices before selling, you could end up with a much higher tax bill.

You pay capital gains taxes for the profit you made from selling an asset. Both the IRS and state governments charge these taxes on major investments. These can cut into the profits you’ve made from selling your home.

There are two types of capital gains taxes: short-term and long-term. Short-term capital gains taxes have higher rates than their long-term counterparts. The lower rates of long-term capital gains taxes are an investor’s ally. By holding onto your assets for longer, you give it time to grow in value and lower its tax burden.

You also simplify the process of calculating your taxes. There are only three brackets for long-term capital gains tax: 0 percent, 15 percent, and 20 percent. Indeed, most people will fall under the 0 percent capital gains tax brackets.

This table outlines the long-term capital gains tax brackets for the 2025 tax season:

| Rate Bracket | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | $0 to $48,350 | $0 to $96,700 | $0 to $48,350 | $0 to $64,750 |

| 15% | $48,351 to $533,400 | $96,701 to $600,050 | $48,350 to $300,000 | $64,751 to $566,700 |

| 20% | $533,401 or more | $600,051 or more | $300,001 or more | $566,701 or more |

| Short-term capital gains are taxed as ordinary income. | ||||

Securing Your Exemptions

Navigating tax cuts for real estate capital gains can be tricky. On one hand, the IRS can be generous with its exclusions. You can exclude up to $250,000 if you are single or married filing separately. Married couples filing jointly can exclude up to $500,000.

For instance, suppose you and your spouse bought a property several years ago for $300,000. By a set of fortuitous circumstances, your property is now worth $850,000. If you sell it, you and your spouse make about $550,000 in profit. Of that amount, you may only pay taxes on $50,000. Property owners who make more modest profits may not pay the IRS anything at all.

But these standard exclusions are contingent on timing and other conditions. You cannot avail of them if you meet any of the following factors:

- The house you sold is not your principal residence.

- You sold a house you only owned for less than two years in the five-year period when you sold it.

- You lived in that house for less than two years in the five-year period when you sold it.

- You’ve claimed a previous IRS exemption on a different property in the past two years before selling your current property.

- You bought the property through a 1031 exchange within the past five years.

- You pay expatriate taxes.

If you meet any of these conditions, you usually must pay taxes on the full amount of your profit. There are a few exceptions. People with disabilities and people in the military, Foreign Service or intelligence community do not need to stay in their homes for two years to qualify for the exemption.

Home Improvement

We’ve already discussed how you can only deduct HELOC costs if you use it to improve upon your home. And that’s not the only tax benefit of home improvement. You may also qualify for capital gains tax breaks when the time comes to sell your home.

Before anything else, remember that the IRS defines “improvement” different from the layperson. Capital improvements must add value to your property. Repair work is usually not counted. They return a home to its original function. Meanwhile, home extensions and other improvements like solar panels could count.

How useful these tax breaks can be varies. People who rely on the standard IRS exemptions can only gain something if their costs were high. It may also not be worth the effort to track your home improvements if you move houses often.

The best candidate for capital improvement tax benefits are people who stay long-term. If your new home appreciates in value significantly, those improvements can help you lower your taxes further.

Other Ways to Save

Improvements aren’t the only expense you can write off to save on taxes upon selling. Most of your other closing costs are also deductible. Many of your selling costs are deductible, be it inspection fees, credit reports, title insurance, attorney’s fees, and agent commissions. You may also write off up to $10,000 in property taxes on that year. No point in getting taxed twice.

As a buyer, you have fewer tax breaks. In the first year, you may only deduct your discount points. But you still have the advantage of writing off your new mortgage’s interest. Other recurring costs you can deduct include mortgage insurance premiums and property taxes.

Most of these deductibles are itemized. Thus, they are only worth taking if they exceed your standard deduction or exclusion. They may be worthwhile for some people but not others. For instance, if you had low costs and only a modest profit, the standard deductions may be enough. If your closing costs are high, itemizing can help offset your expenses.

A tax return is money you were supposed to keep in the first place. An effective tax management strategy is key to ensuring that you pay only your fair share.

El Monte Borrowers: Are You Unsure Which Loans You'll Qualify For?

We have partnered with Mortgage Research Center to help El Monte homebuyers and refinancers find out what loan programs they are qualified for and connect them with El Monte lenders offering competitive interest rates.