How Does Advertised APR Compare Against Real APR?

It can cost lenders around $7,000 to originate a mortgage loan. To help recoup these costs they can charge the borrow a higher interest rate, sell discount points, or charge other fees like loan origination points and other closing costs. This calculator makes it easier to compare like with like to see the actual APR for loans with different point totals or other closing costs by merging these other expenses into the effective interest rate.

Real Annual Percentage Rate Calculator

Unsure if your loan is a good deal? Want to know the full cost? To discover the real APR of your loan, enter your loan amount, interest rate, points, additional closing costs, and loan term. We will then tell you what the real APR is with those costs blended into your loan's rate.

We publish current El Monte mortgage rates to help you compare any quoted rates you received against competitive rates from our online network of mortgage lenders.

The Real APR on Your $320,000 Home Loan is 7.24%

| Stated Loan Amount | Effective Loan Amount |

|---|---|

$2,128.97Monthly Payment |

$2,179.53Monthly Payment |

Advertised Rate |

Annual Percentage Rate (APR) |

7% |

7.24% |

Current El Monte Mortgage Rates on $320,000 Home Loans

The following table highlights current El Monte mortgage rates. By default 30-year purchase loans are displayed. Clicking on the refinance button switches loans to refinance. Other loan adjustment options including price, down payment, home location, credit score, term & ARM options are available for selection in the filters area at the top of the table.

Mortgage APR and its Importance to Homeowners

You may have heard the term annual percentage rate (APR) if you’ve been shopping for a home. But did you ever stop to think what it’s for? How does it differ from the interest rate on your mortgage? The reality is complex, but APRs are designed to make life easier for borrowers.

The APR is a simple way of comparing deals offered by various lenders. Comparing offers from different lenders is like comparing apples and oranges. You need a separate yardstick for each. Think of the APR as a pair of magical glasses. Through this lens, you can see all lenders and financing deals on an equal field. You can even use it to compare mortgage options from the same lender.

The Lowdown on Mortgage APR

What’s the difference between an interest rate and an APR? The interest rate is the cost of borrowing money. This calculates how much you must pay your lender for the use of their money. A 3 percent interest rate means you must pay 3 cents for every dollar you borrow.

An APR, meanwhile, calculates the true cost of your debt over a yearly basis. Besides interest, it factors in closing costs, points, and origination fees. It does not include application fees, late payment penalties, or fees for property appraisals and document preparation. Note that your loan’s APR is usually higher than the advertised rate.

The rates as advertised are often not the same rate that applies to your mortgage payments. Hence, they are known as nominal rates. They often seem like a good deal on the surface. Meanwhile, your APR is the functional rate that applies to your monthly payments. It reflects the reality of your mortgage.

Through the Truth in Lending Act, the government insists that lenders make this information available. When you apply for a mortgage, the lender must make you aware of both figures. The law forbids lenders from emphasizing one rate over the other. Look at both numbers up close to understand your mortgage and the obligations it entails.

Through a Different Lens

Picture your prospective lenders all lined up in a row. They will all have shiny, tempting offers to try and win your business. Some will have lower rates, but add points. Others will offer no points and low interest rates. But these lenders will charge high fees. A few less scrupulous lenders will try and dazzle you with deceptive offers. Their pitches will be lined with bait-and-switch tactics, misleading claims, and attractive promises.

Now, look at these through the lens of APR. Once you know the loan’s APR, the flowery marketing promises fade away. The APR lets you see mortgage expenses for what they are. What seems like a good deal may be the most expensive one of the bunch. It lets you compare these categories side by side. Armed with this knowledge, you’ll know what these offers mean for your bank account in the long run.

The APR also shows your money’s real buying power. Want to know if paying more upfront in exchange for a lower rate is worth it? Your loan’s APR will be the judge of that.

Calculating Your APR

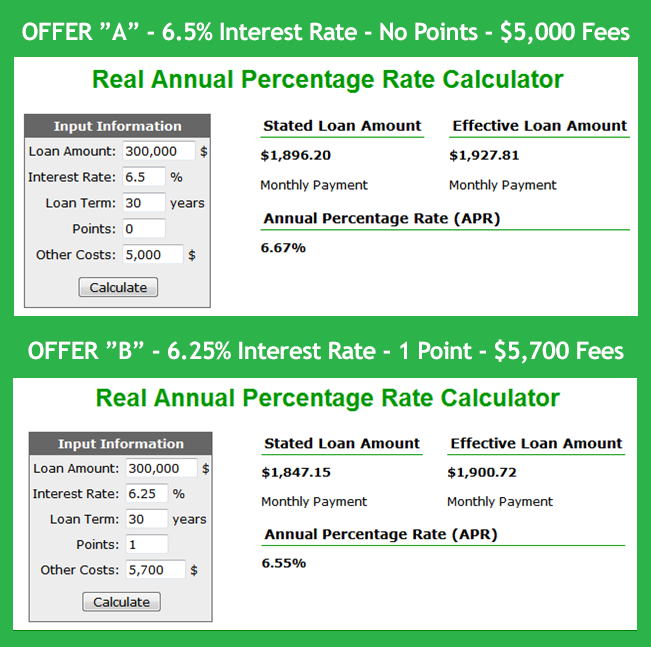

Finding your APR entails a complex mathematical operation. This process takes into account origination fees, mortgage points, and mortgage insurance. Using the above calculator, let’s find out how two different mortgage offers measure up.

In our example, you go to two lenders with the same type of mortgage for a house worth $375,000. You pay a 20 percent down payment worth $75,000, and borrow a principal worth $300,000. In both instances, you sign up for a 30-year fixed-rate term.

The first potential lender offered a 6.5 percent deal with no upfront points. Their fees cost around $5,000. Each point is equal to 1% of the principal. The second lender, meanwhile, offers a rate of 6.25 percent. They ask for one point as part of the deal and charge $5,700 in extra fees.

Let’s see which of the two has the lower monthly payment and APR:

30-Year Fixed-Rate Mortgage

Principal: $300,000

| Category | Offer A | Offer B |

|---|---|---|

| Nominal Rate | 6.5% | 6.25% |

| Points | 0 | 1 |

| Other Costs | $5,000 | $5,700 |

| Stated Monthly Payment | $1,869.20 | $1,847.15 |

| Effective Monthly Payment | $1,957.81 | $1,900.72 |

| APR | 6.67% | 6.55% |

The second offer is the better deal based on APR alone. You pay less each month and cut down on your interest costs in the long run. It seems simple enough to understand. Moreover, this assumes you’ll be staying in your home for the full 30 years. In financing a home, things are not always that clean cut.

Monthly Payments

A mortgage with lower monthly payments isn’t always the cheaper option. A 30-year fixed-rate mortgage is popular with American homebuyers because it has lower monthly payments. But since payments are spread out over a longer period of time, it costs you more in interest. Lenders charge lower rates for 15-year fixed-rate mortgages. Your functional APR and your total costs are lower, but you pay a higher monthly payment with a short term. However, you’ll spend significantly less interest charges if your term is 15 years compared to a 30-year loan.

Complicating Factors

As the saying goes, time equals money. It is a key variable in establishing payments and amortization schedules. In general, the longer your amortization schedule, the cheaper your monthly payments. However, it also means you pay more in interest charges. And that isn’t the only factor at play.

To make points worthwhile, you must live in the property for a long time to spend less on it. People who plan to live in their homes long-term can save money through discount points. Paying more in interest today will reduce your costs tomorrow. Over time, you’ll recoup your costs and reap the benefits of a lower APR.

Let’s return to our example. All things being equal, the second option seems like the best deal. But first, you must also ask yourself the following questions:

- Do you have enough cash to cover the closing cost and points?

- Will you live for the next 15 or 30 years in your home?

If you answer “yes” to both these questions, then the second option is indeed the better one. But what if you don’t have the closing costs and the points? What if you plan to move in a few years? In that case, the first option (which costs less up-front) is the better deal for you.

Limitations

The Federal government also sets limits to APRs to protect consumers. These caps prevent lenders from imposing usuriously high rates to borrowers. It also discourages predatory lenders from trapping homeowners in toxic debt cycles. Both the APR and its limitations are valuable tools geared to protecting the consumer.

Mortgage Discount Points

Because of competition, lenders often have very similar offers on the surface. They try to sweeten the pot by lowering their advertised interest rates. Some do this by charging borrowers with an upfront fee for the privilege. These are called discount points. Purchasing discount points can be an effective long-term investment. You pay in advance now to avoid more interest costs in the future.

Most discount points usually cost 1 percent of your principal. For instance, if you borrowed $300,000, each mortgage point will cost you $3,000. Buying two mortgage points would cost $6,000. In most cases, a point reduces the effective interest rate by a quarter of a percentage. However, note that lenders may define charges for points differently.

You have two ways to pay for points. The straightforward method is to pay for them out of pocket. This can be costly upfront, especially with other closing costs to cover. The other is to finance them into your mortgage. While this lets you buy them and save money today, it increases your principal, which raises your monthly payments.

Points make the best sense when used on a fixed-rate mortgage. They lower the effective interest rate through the loan’s entire lifetime. Points on an adjustable-rate mortgage (ARM), meanwhile, usually only lower the introductory rate during the initial teaser period. Afterward, your rate will float at a margin against the referenced index rate through your amortization period.

Here is an example of how points operate. In this table below, we assume a 30-year fixed-rate mortgage with a balance of $300,000. Your lender gives you a nominal rate of 5.5 percent and offers two discount points:

30-year Fixed-Rate Mortgage

Principal: $300,000

Nominal Rate: 5.5%

| Category | No Points | 1 Discount Point | 2 Discount Points |

|---|---|---|---|

| Cost | $0.00 | $3,000.00 | $6,000.00 |

| APR | 5.5% | 5.25% | 5% |

| Monthly P&I Payment | $1,703.37 | $1,656.61 | $1,610.46 |

| Monthly Payment Savings | N/A | $46.76 | $86.91 |

| Months to Recover Point Cost | N/A | 64 (5 years, 3 months) | 69 (5 years, 9 months) |

| Savings Over 30 Years | N/A | $13,833.60 | $25,287.60 |

It seems that buying two discount points saves you the most money. But notice that it takes more than five years to break even. Your largest savings depend on staying in your home throughout the amortization period.

Discount points make sense for people who are certain they will live in the home for an extended period. They must live in the house long enough not only to recoup their upfront costs, but also to save money on interest. However, the points do not make sense if you sell your home within a short span of time, such as less than 5 years. In this case, you may end up losing thousands of dollars buying points. Meanwhile, buying points today may also be cheaper than refinancing your mortgage tomorrow. If you do refinance, you may even buy points to lower your rates further.

Tax Advantages

For tax purposes, a discount point is prepaid mortgage interest. It is thus eligible for tax deductions in the year the loan is originated.

Private Mortgage Insurance

Private mortgage insurance (PMI) applies to conventional mortgages with a loan-to-value (LTV) ratio greater than 80 percent. Your LTV ratio is the percentage of your home financed by the bank. The lower your starting LTV, the more of your home you own outright. If you pay less than a 20 percent down payment on a conventional mortgage, you must pay PMI premiums, which is rolled into your monthly payments. The cost of PMI can range between 0.5 percent to 2 percent of your loan amount per year.

Lenders perceive borrowers with higher LTV ratios as riskier. Thus, they compel the borrower to pay for PMI coverage. Despite its name, this mortgage insurance does not protect you at all. It hedges your lender against the possibility of you defaulting on your mortgage.

By law, PMI payments last until your principal balance falls to 78 percent of your home’s value. You may ask lenders to remove your PMI after your balance reaches 80 percent. Often, you must keep track of these numbers yourself.

Let’s return to our previous example. Suppose you had a 0.5 percent PMI rate for a $300,000 mortgage. Each year, it will cost you $125 each month until your LTV falls to about 78 percent. And this could take a couple of years. In effect, it will raise your APR. Avoiding PMI is the most sensible thing you can do as a borrower. It offers no benefit and will linger for some time. If you can, focus on avoiding PMI over shouldering other expenses.

Let’s assume that your present down payment is close to 20 percent. If you buy points, however, it will dip well below that. In this case, you are better off increasing your down payment to 20 percent rather than buying points.

Mortgage Insurance Premiums and Funding Fees

Government-backed mortgages have different forms of lender insurance associated with them. Loans sponsored by the Federal Housing Authority (FHA) and the U.S. Department of Agriculture (USDA) come with mortgage insurance premiums (MIPs). These consist of an upfront insurance fee on the closing of your mortgage and an annual fee thereafter. Unlike PMI, you cannot get rid of MIPs by reaching a LTV ratio threshold. For instance, 30-year fixed rate FHA loans require MIP for the entire mortgage term. To remove MIP, you must often refinance into a conventional mortgage.

Loans backed by the Department of Veterans Affairs (VA), meanwhile, have a one-time funding fee. You can roll this fee into your principal or pay for it upfront. Funding fees are based on your down payment, whether you’ve used your VA benefit before, and the type of VA loan you get.

Origination Fees

Unlike mortgage points, other upfront loan origination fees are not tax deductible. Lenders charge these for completing your mortgage application. In the U.S., their costs often range between 0.5 and 1 percent of your principal. For example, if your loan amount is $350,000, a 1% origination fee would cost $3,500. Be sure to set aside budget for this expense.

In the past, lenders had fewer limits to how much they could charge in origination. Predatory subprime lenders charged borrowers with exuberant origination fees. These often surpassed 4 percent of your mortgage principal. In the wake of the 2008 Financial Crisis, consumer protection regulations have since restricted excessive fees.

On the opposite end, some lenders may advertise loans with a 0 percent origination fee. This is not always the bargain that it seems. Origination fees are transparent upfront charges. You pay only so much to close your mortgage. But lenders who don’t charge origination fees shift this cost into the interest. In essence, you end up with half a negative point baked into your interest rate.

Lower upfront costs often lead to higher total expenses. Suppose your lender offers no origination fees for a mortgage with a rate of 5.75 percent. Another mortgage with upfront origination fees may have an effective APR of 5.5 percent.

Other Fees

Not all fees that apply to your mortgage influence your APR. Most real estate transactions also have appraisal, title, and recording fees. You also have monthly escrow expenses like property taxes and homeowner’s association fees. You needn’t consider these expenses when determining your APR.

This is because they are external fees. They are not associated with your mortgage at all. You pay these to people other than your lender. While they are often part of your monthly payment, your taxes and HOA fees are deposited into an escrow account. You will still pay for them even if you finance your home out of pocket. So make sure to add these costs when budgeting your mortgage expenses.

In Summary

Homes are among the biggest financial investments made by most consumers. Buyers must make sure they are getting the best mortgage deal at all steps of the process. But this task is easier said than done.

Lenders vary with what they offer, which can be overwhelming and confusing. The differences are often subtle because many banks have similar cost of capital. This leads them to offer similar quotes for borrowers of a given risk profile. Look closely at each offer. While they appear the same, their variations have a profound effect on your total costs. Thus, the APR is invaluable in helping you make sense of the confusing world of housing finance.

Remember, the APR is a tool. While it is essential in comparing the true cost of your mortgage options, it can’t make the answers for you. Consider other factors like how long you’ll live in the house and closing costs. The best option for you may not always be the one with the lowest APR. It is the one that gives you the most savings based on your life goals and current finances.

El Monte Borrowers: Are You Unsure Which Loans You'll Qualify For?

We have partnered with Mortgage Research Center to help El Monte homebuyers and refinancers find out what loan programs they are qualified for and connect them with El Monte lenders offering competitive interest rates.